April 2024 | Drama Is Not A Strategy

Dramatic headlines sell.

We have all seen the dire predictions of a deep recession and market collapse as a result of the Federal Reserve increasing the Federal Funds Rate from near zero to the current range of 5.25-5.50%. Our view remains that while the rate of increase has certainly been dramatic, interest rates are now roughly in line with long-term averages, and manageable for the economy.

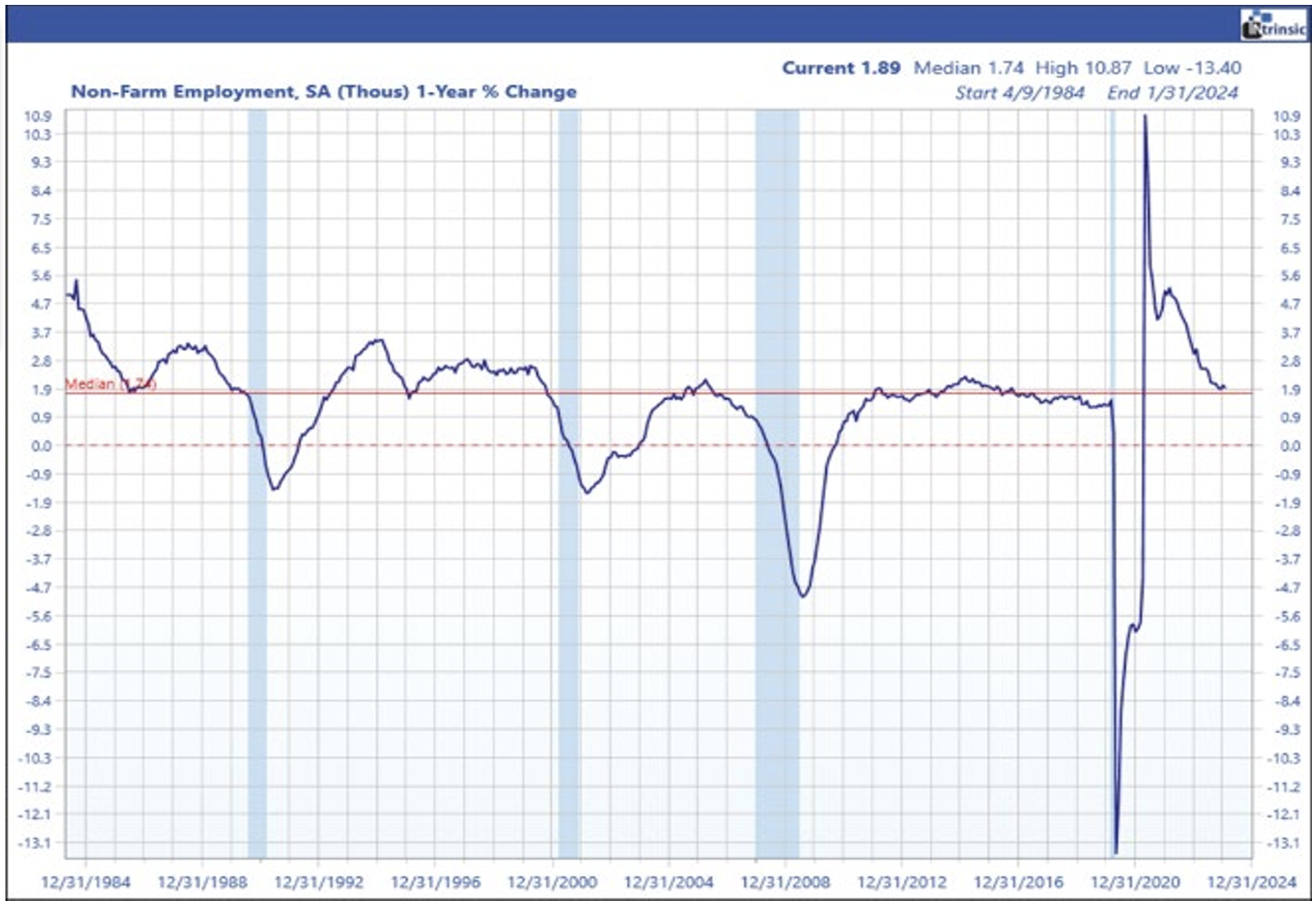

The Covid Pandemic and the ensuing government responses created unprecedented swings in the economy and markets – this was true drama. Consequently, many past precedents didn’t seem to apply as measure after measure blew through historical norms. Two examples are illustrated in the accompanying charts. At left, employment tanked and then rebounded dramatically, as the economy was essentially shut down when the pandemic hit and then restarted when vaccines arrived. (1*,2*)

Similarly, consumer spending virtually stopped as people feared for their jobs and were quarantined in their homes, then stormed back thanks to government stimulus and the eventual return to work.

These charts and many more like them certainly paint a dramatic picture, but the more salient point to us is the current readings, as both have returned to median levels. We see this pattern repeated in chart after chart from the last four years. The economy has normalized and we see GDP doing the same, settling near its historical median of 2.6% annual growth. (3*)

While the economy reflects a return to normalcy, the S&P 500 Index suggests the stock market is a bit extended. (4*) Given the rise in the index over the last 15 months, this is not particularly surprising. The chart below shows the price of the index above and the median price/earnings ratio below. (5*) At current levels, the S&P appears a bit overvalued. Some caution related to equities is warranted.

Regarding interest rates, the current effective Fed Funds rate of 5.3% is slightly above its 50-year median of 4.8%, suggesting there is room for rates to decline a bit in the quarters to come. The Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditures Index (PCE) has declined from a high of 5.5% in March 2002, to its latest reading of 2.8%. This is down substantially, but still above the Fed’s 2% target. Given the underlying strength of the economy and the fact that interest rates across the board are close to their long-term medians, we would expect any rate cuts from the Fed to be small and gradual.

The U.S. economy is a remarkable machine. Following unprecedented upheaval and equally novel responses, the diversity and dynamism of the world’s largest economy has allowed for a return to a reasonable equilibrium. This is not to say we won’t have further periods of high drama, but it does suggest that maintaining a balanced, diversified portfolio is the appropriate approach for long-term investors. Drama makes headlines, but patience brings returns.

— Brad Dinsmore

1. 2. 3. Charts sourced from Intrinsic

4. The S&P 500 Index is a market-capitalization weighted index that includes the 500 most widely held companies chosen with respect to market size, liquidity, and industry. You cannot invest directly in an index. Indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees.

5. Chart sourced from Ned Davis Research